The United States (US) Bureau of Labor Statistics (BLS) will release the Nonfarm Payrolls (NFP) data for May on Friday at 12:30 GMT.

With Fed policymakers becoming more hawkish as the new Chairman Kevin Warsh takes the helm, investors will scrutinize the underlying details of the employment report to assess whether the Federal Reserve (Fed) will lean toward a tighter policy later in the year.

US payrolls are among the most market-moving indicators. Still, this time, with all eyes on the inflation front, only a dismal print will be able to significantly hit the US Dollar.

What to expect from the Nonfarm Payrolls report?

Investors expect NFP to rise by 85K following the surprisingly strong 185K and 115K increases recorded in March and April, respectively. The Unemployment Rate is seen holding steady at 4.3%, while the annual wage inflation, as measured by the change in the Average Hourly Earnings, is projected to soften to 3.4% from 3.6% in April.

Previewing the employment report, TD Securities analysts note that they expect NFP to register its lowest gain in three months at 60K in May.

“Gains will stem from the private sector, as we expect government jobs to be flat. We also anticipate the Unemployment Rate rate will edge higher for a second consecutive month to 4.4% [above the broader consensus of a stable 4.3%], assuming the participation rate stays largely unchanged. Average Hourly Earnings likely picked up 0.3% m/m (3.5% y/y),” they add.

Automatic Data Processing (ADP) reported earlier in the week that employment in the private sector rose by 122K in May. This print followed the 105K (revised from 109K) increase reported in April.

“Hiring was more broad-based in May than we’ve seen in the last few years. The labor market continues to show sustained momentum going into the summer hiring season,” said Nela Richardson, Chief Economist at ADP.

Meanwhile, the Employment Index of the Institute for Supply Management’s (ISM) Manufacturing Purchasing Managers’ Index (PMI) improved to 48.6 from 46.4 in April, while the Employment Index of the ISM Services PMI was virtually unchanged at 47.9. Still, with both readings remained in the contraction territory, contradicting the ADP’s findings.

How will the US May Nonfarm Payrolls affect EUR/USD?

The US Dollar (USD) has been benefiting from the risk-averse market environment due to a prolonged crisis in the Middle East. Additionally, growing fears over high energy costs leading to persistently strong inflation have been paving the way for a hawkish Federal Reserve (Fed) policy pricing, further supporting the currency.

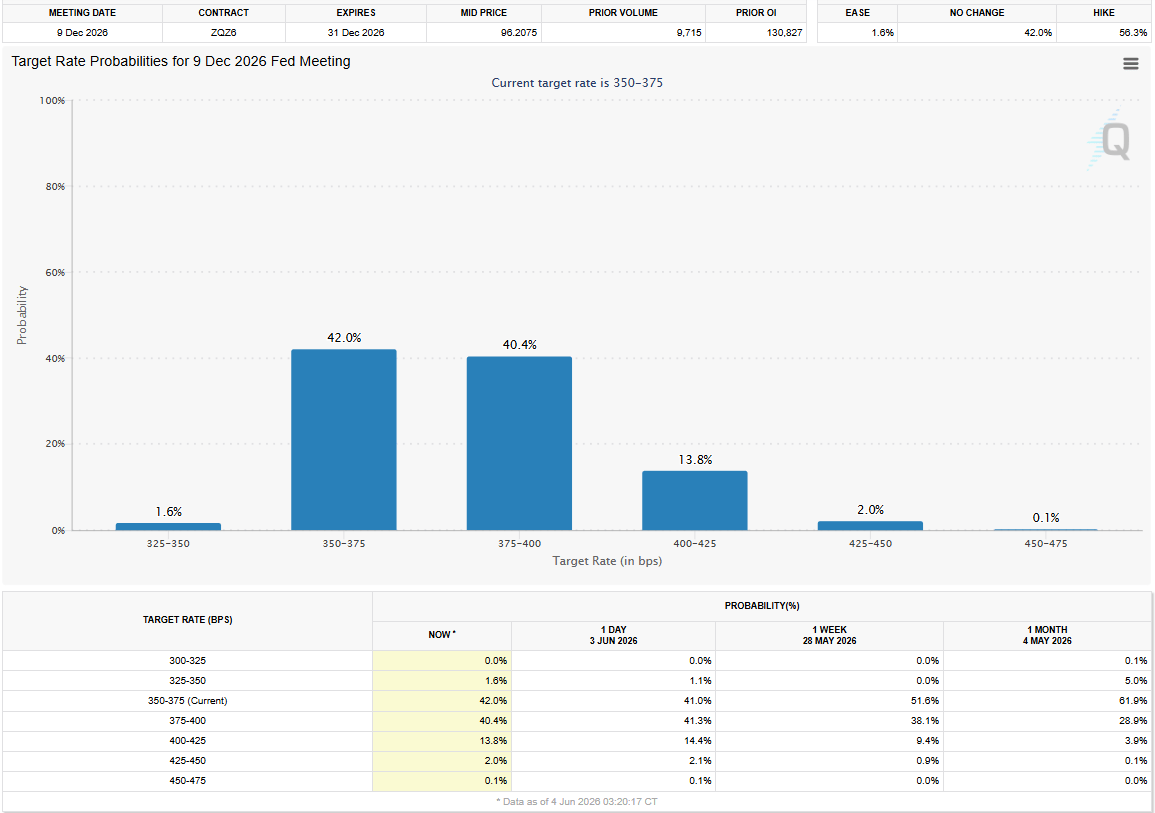

After rising about 0.9% in May, the USD Index is up 0.5% so far in June, while markets see a nearly 60% probability of the US central bank raising the policy rate by 25 basis points (bps) at least once by the end of 2026, as per CME FedWatch Tool.

Unless there is a significant downside surprise in the headline NFP print, policymakers are likely to focus on taming inflation without worrying about labor market conditions.

Dallas Fed President Lorie Logan said earlier this week that the labor market is stable and noted that inflation is taking too long to return to 2%. “I am increasingly concerned that higher interest rates could be necessary later this year,” Logan added.

Similarly, New York Fed President John Williams stated that the job market is healthy and upside risks to inflation have increased. Furthermore, Cleveland Fed president Beth Hammack said that the Fed may need to act soon if inflation trends don’t cool and echoed the same sentiment about employment conditions, noting that “job market data point to stability.”

Overall, Fed policymakers are largely tilting toward the hawkish side due to persistent inflation pressures and signs that the labor market is holding up well.

Following two consecutive months of robust readings, a figure above 50K could be seen as a “good enough” growth in NFP. In this scenario, the USD could gather strength heading into the weekend and cause EUR/USD to stretch lower.

At this point, only consecutive dismal NFP figures could sway policymakers’ view about the policy outlook. Hence, even if the NFP data comes in below 50K, any negative impact on the USD could remain short-lived. While EUR/USD could gain traction with the immediate reaction, a steady recovery could be difficult to come by.

In summary, the USD shouldn’t have a hard time staying resilient against its peers in the near future.

A single disappointing NFP print might not be enough to shift the market conviction about a tighter Fed policy. Only a reopening of the Strait of Hormuz, whether by an extended ceasefire or a truce deal between the US and Iran, could trigger a deep correction in crude Oil prices and ease inflation concerns. In this market environment, this seems to be the only possible scenario in which the USD enters a bearish trend and opens the door to a decisive rally in EUR/USD.

Eren Sengezer, European Session Lead Analyst at FXStreet, offers a brief technical outlook for EUR/USD:

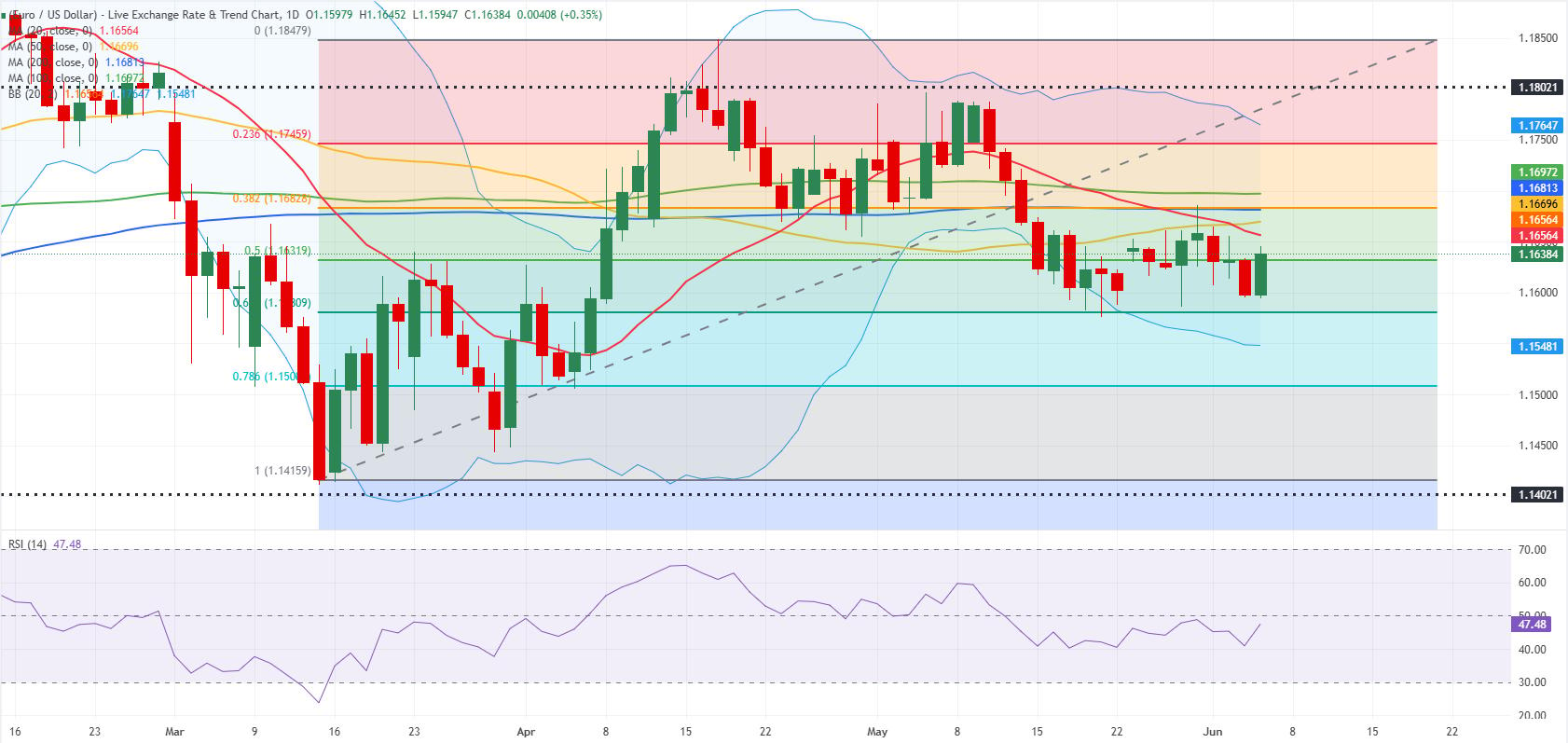

“EUR/USD’s near-term technical outlook suggests that the bearish bias stays intact but lacks momentum. The Relative Strength Index (RSI) indicator on the daily chart remains slightly below 50 after testing 40 and the pair stays in the lower half of Bollinger Bands, while trading below all key Simple Moving Averages (SMA).”

“On the downside, 1.1580 (Fibonacci 61.8% retracement of the mid-March – Mid-April recovery) aligns as an interim support level before 1.1500 (Fibonacci 78.6% retracement) and 1.1415-1.1400 (static level, March 13 low).”

“Looking north, a strong resistance area could be spotted at the 1.1680-1.1700 region, where the 200-day SMA, 100-day SMA and the Fibonacci 38.2% retracement level align. In case EUR/USD stabilizes above this region, it might be able to attract technical buyers and target 1.1750 (Fibonacci 23.6% retracement) ahead of 1.1800 (static level, round level).”

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money.

When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions.

The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Read the full article here