The European Central Bank (ECB) is set to announce its monetary policy decision at 12:15 GMT following its June meeting.

The Frankfurt-based institution is widely expected to raise its key interest rates by 25 basis points, taking the deposit facility rate to 2.25% from 2%. Such a move would mark the first rate hike since September 2023 and reflect policymakers’ growing concern about the inflationary impact of the energy shock caused by the war in Iran and the disruption of shipping routes in the Middle East.

ECB President Christine Lagarde will hold a press conference shortly after the announcement, at 12:45 GMT, where investors will seek guidance on whether June represents the start of a broader tightening cycle or merely a precautionary adjustment. The ECB is expected to publish updated staff projections alongside the decision, with economists anticipating higher inflation forecasts and weaker growth estimates compared with the March projections.

While a rate hike is largely priced in by financial markets, uncertainty remains elevated. Policymakers must balance the risk of inflation becoming more persistent against the danger of further weakening an already fragile Eurozone economy. As a result, communication regarding future policy steps is likely to be the key market driver.

What to expect from the ECB interest rate decision?

The ECB enters the June meeting facing a significantly different environment than it did only a few months ago. Eurozone inflation accelerated to 3.2% YoY in May from 3% in April, while core inflation rose to 2.5%, reflecting the gradual transmission of higher energy prices into broader price categories.

Several Governing Council members have openly supported a rate increase in recent weeks. ECB Chief Economist Philip Lane indicated that inflation projections would likely be revised higher, while Executive Board member Isabel Schnabel argued that the central bank could no longer simply “look through” the energy shock. Even traditionally dovish policymakers have acknowledged that a tightening of monetary policy may be necessary to prevent inflation expectations from becoming unanchored.

Updated ECB projections are expected to reinforce this view as several institutions forecast that inflation estimates for 2026 could be revised closer to 3%, up from 2.6% in March, while growth forecasts are likely to be downgraded as higher energy costs weigh on activity. Recent Purchasing Managers Index (PMI) surveys have already pointed to deteriorating business conditions, with Eurozone economic activity remaining in contraction territory.

Despite the expected hike, the ECB is unlikely to provide explicit forward guidance. Policymakers continue to emphasize a data-dependent and meeting-by-meeting approach, reflecting the exceptional uncertainty surrounding the geopolitical situation and future energy prices. Most analysts expect Christine Lagarde to maintain a cautiously hawkish tone, acknowledging upside risks to inflation while avoiding any commitment regarding the timing of additional moves.

The key debate within markets is whether June marks the beginning of a new tightening cycle or simply an insurance hike designed to preserve the ECB’s anti-inflation credibility. While some institutions foresee multiple hikes over the coming months, others argue that weakening growth, tighter financial conditions and limited evidence of wage-driven inflation should ultimately restrict the scope of further tightening.

How could the ECB meeting impact EUR/USD?

Ahead of the decision, markets have largely priced in a 25-basis-point rate increase, meaning the Euro’s immediate reaction may depend more on the ECB’s communication than on the decision itself.

A more hawkish-than-expected message from Christine Lagarde, particularly if she suggests that additional rate hikes could be warranted in July or September, would likely support the Euro (EUR) by pushing European rate expectations higher. An upward revision to inflation forecasts that highlights persistent price pressures could further reinforce this reaction.

Conversely, if the ECB emphasizes downside risks to growth and signals that June should not be interpreted as the start of an aggressive tightening cycle, the common currency could struggle to gain traction despite the rate increase. Traders would likely interpret such communication as confirmation that only limited additional tightening remains likely.

Interest rate differentials will remain a key driver for EUR/USD. While the ECB is expected to raise rates this week, the Federal Reserve (Fed) is widely expected to keep policy unchanged at its upcoming meeting, even as markets start to anticipate rate hikes later this year. This divergence could provide near-term support for the Euro if the ECB adopts a sufficiently hawkish tone.

Nevertheless, broader market themes remain highly influential, as developments in the Middle East conflict, energy markets and global risk sentiment could continue to dominate EUR/USD price action. As a result, unless the ECB substantially alters expectations regarding the future path of interest rates, the pair may remain driven as much by geopolitical developments as by monetary policy itself.

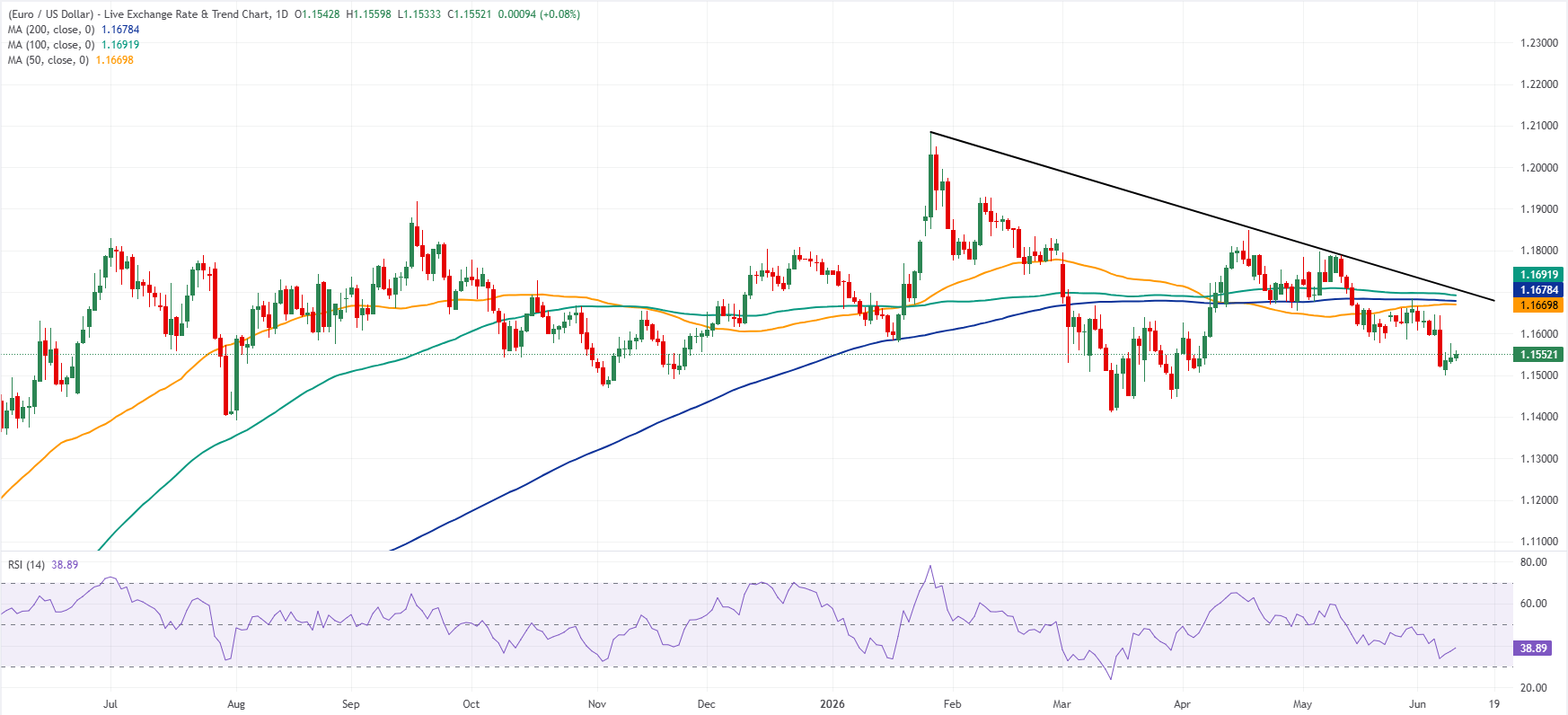

Since early June 2025, the EUR/USD pair has been trading within a broad horizontal range, with no clear trend. In the daily chart above, EUR/USD maintains a bearish near-term tone as spot remains anchored below the 50-day, 200-day and 100-day Simple Moving Averages (SMAs), clustered between roughly 1.1670 and 1.1692.

The downward resistance trend line, last intersected around 1.1704, continues to frame the broader downside bias. Meanwhile, the Relative Strength Index (RSI) at 38.9 indicates weak momentum but stops short of oversold territory, suggesting that sellers retain control, albeit with limited immediate exhaustion signals.

On the topside, initial resistance emerges at the 50-day SMA near 1.1670, followed closely by the 200-day SMA around 1.1678, creating a dense supply band just overhead. A move above these would then expose the 100-day SMA at 1.1692 ahead of the trend-line reference near 1.1704.

On the downside, the first support comes at the psychological 1.1500 level, close to Monday’s low. A break below this area could reinforce the bearish pressure and open the door for a move toward 1.1400, a key support zone located near the March 13 and August 1 lows. A sustained decline below 1.1400 would further strengthen the negative outlook and expose lower levels not seen since June 2025.

(The technical analysis of this story was written with the help of an AI tool.)

Economic Indicator

ECB Rate On Deposit Facility

One of the European Central Bank’s three key interest rates, the rate on the deposit facility, is the rate at which banks earn interest when they deposit funds with the ECB. It is announced by the European Central Bank at each of its eight scheduled annual meetings.

Read more.

Next release:

Thu Jun 11, 2026 12:15

Frequency:

Irregular

Consensus:

2.25%

Previous:

2%

Source:

European Central Bank

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

Read the full article here