At the post-meeting press conference, Fed Chair Jerome Powell explained why policymakers decided to keep interest rates unchanged following the March meeting and took questions from reporters on the decision.

Powell’s press conference highlights

The economy is expanding.

Inflation remains somewhat elevated.

The current policy stance is appropriate and supports progress towards our goals.

We will remain attentive to risks on both sides of the mandate.

Consumer spending remains resilient, while housing sector activity is weak.

Labour demand has clearly softened.

We estimate February PCE inflation at 2.8%, with core PCE at 3.0%.

Elevated inflation largely reflects goods.

Near-term inflation expectations have risen, while longer-term expectations remain consistent with the 2% goal.

Recent rate cuts have brought policy closer to a plausible estimate of neutral.

The implications of developments in the Middle East remain uncertain

Higher energy prices will push up inflation in the near term.

It is too soon to know the scope and duration of these effects.

We are well positioned to determine future rate adjustments.

Policy is not on a preset course and decisions will be taken meeting by meeting.

The projections are not a plan and are subject to uncertainty.

A number of policymakers have shifted towards fewer rate cuts.

We expect progress on inflation to continue, but less than previously hoped.

Progress on goods inflation will be key to assessing further disinflation.

We will not take lightly the decision to look through energy-driven inflation.

If inflation progress stalls, rate cuts will not follow.

The economy is expanding and doing pretty well.

Inflation remains somewhat elevated, with recent progress slower than hoped.

The current policy stance is appropriate and is at the high end of neutral, or mildly restrictive.

We will remain attentive to risks on both sides of the mandate.

Consumer spending remains resilient, while housing activity is weak.

Labour demand has clearly softened and the labour market is not a source of inflationary pressure.

Recent inflation overshoot is mainly driven by goods and tariffs.

Near-term inflation expectations have risen, while longer-term expectations remain anchored at 2%.

Higher energy prices will push up inflation in the near term, but the effects remain uncertain.

No one knows the economic impact of the Middle East conflict.

We will not take lightly the decision to look through energy-driven inflation.

Progress on goods inflation is key to assessing further disinflation.

We expect inflation to improve, but less than previously hoped and it may take more time.

A number of policymakers have shifted towards fewer rate cuts.

Policy is not on a preset course and decisions will be taken meeting by meeting.

If inflation progress stalls, rate cuts will not follow.

The vast majority of participants do not see a rate hike as the base case, but risks to policy are two-sided.

We do not want policy to become too restrictive given downside risks to the labour market.

Job creation is very low, and a zero-growth equilibrium carries downside risks.

Inflation expectations must remain anchored and will be monitored very carefully.

Growth projections reflect increasing confidence in productivity.

This is not stagflation, but rather a balance between the two sides of the mandate.

I would not say I am certain that tariffs will be a one-time effect.

Inflation is an ongoing increase in prices, not a one-time adjustment, and in theory tariffs should be a one-time effect.

We do not know how long it will take for tariffs to pass through the economy.

We have slightly more confidence that tariff-related inflation will ease around the middle of the year.

People feeling squeezed is a very real issue, and it reinforces our commitment to bringing inflation back down.

The upward revision in growth projections reflects stronger productivity.

This section below was published at 18:00 GMT to cover the Federal Reserve’s policy decisions and the immediate market reaction.

At its March meeting, the Federal Reserve (Fed) kept its Fed Funds Target Range (FFTR) unchanged at 3.50%–3.75%, right in line with what markets were expecting.

Highlights from the FOMC statement

The Federal Reserve left the policy rate unchanged at 3.50% to 3.75%.

Uncertainty about the economic outlook remains elevated.

Available indicators suggest that economic activity has been expanding at a solid pace.

Job gains have remained low and the unemployment rate has been little changed in recent months.

Inflation remains somewhat elevated.

The Committee is attentive to risks to both sides of its dual mandate.

The implications of developments in the Middle East for the US economy remain uncertain.

The vote was 11 to 1, with one member favouring a 25 basis point rate cut.

Key takeaways from the Summary of Economic Projections (SEP)

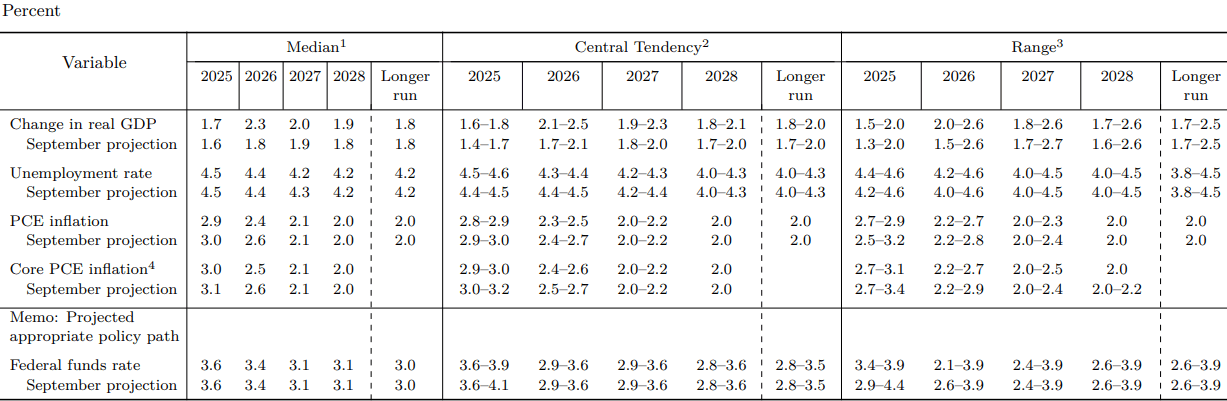

The median projection for the policy rate at the end of 2026 stands at 3.4%

The median projection for the policy rate at the end of 2027 stands at 3.1%

The median projection for the policy rate at the end of 2028 stands at 3.1%.

The longer-run policy rate is seen at 3.1%.

The projections imply around 25 basis points of rate cuts in 2026 and a further 25 basis points in 2027.

Several policymakers see no rate cuts in 2026, while one sees rates higher in 2027.

The unemployment rate is projected at 4.4% at the end of 2026.

PCE inflation is projected at 2.7% in 2026, with core PCE also seen at 2.7%.

GDP growth is projected at 2.4% in 2026, with longer-run growth seen at 2.0%.

Market reaction to Fed policy announcements

The US Dollar keeps pushing higher on Wednesday, extending its rebound after two consecutive daily pullbacks. That said, the US Dollar Index (DXY) refocuses its attention to the psychological 100.00 barrier, while higher US Treasury yields across the curve also underpin the move following the Fed’s interest rate decision.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.20% | 0.10% | 0.21% | 0.08% | 0.32% | 0.25% | 0.65% | |

| EUR | -0.20% | -0.09% | 0.02% | -0.11% | 0.11% | 0.03% | 0.44% | |

| GBP | -0.10% | 0.09% | 0.11% | -0.04% | 0.21% | 0.13% | 0.52% | |

| JPY | -0.21% | -0.02% | -0.11% | -0.14% | 0.12% | 0.02% | 0.40% | |

| CAD | -0.08% | 0.11% | 0.04% | 0.14% | 0.24% | 0.16% | 0.56% | |

| AUD | -0.32% | -0.11% | -0.21% | -0.12% | -0.24% | -0.08% | 0.32% | |

| NZD | -0.25% | -0.03% | -0.13% | -0.02% | -0.16% | 0.08% | 0.39% | |

| CHF | -0.65% | -0.44% | -0.52% | -0.40% | -0.56% | -0.32% | -0.39% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

This section below was published at 10:00 GMT as a preview of the Federal Reserve’s policy announcements.

- The US Federal Reserve is expected to leave the policy rate unchanged for the second consecutive meeting.

- The Summary of Economic Projections will offer key insights into policy outlook as markets fear an inflation comeback due to the spike in energy prices.

- Fed Chair Powell’s comments could ramp up USD volatility as the Iran war has sharply reduced expectations for rate cuts this year.

The United States (US) Federal Reserve (Fed) announces its interest rate decision on Wednesday, a pivotal meeting for markets to gauge the stance of the world’s most important central bank after an energy shock that could put the Fed’s dual mandate in tension. While the main decision on interest rates is a given, the surge in Oil prices after the Iran war adds a layer of uncertainty that could turn this meeting into much more interesting – and more volatile for markets – than initially expected.

Markets widely expect the Federal Open Market Committee (FOMC) to keep the policy rate unchanged in the range of 3.5%-3.75% for the second consecutive meeting.

As this decision is nearly fully priced in, the Summary of Economic Projections (SEP) and Fed Chair Jerome Powell’s comments in the post-meeting press conference could impact the US Dollar’s (USD) performance.

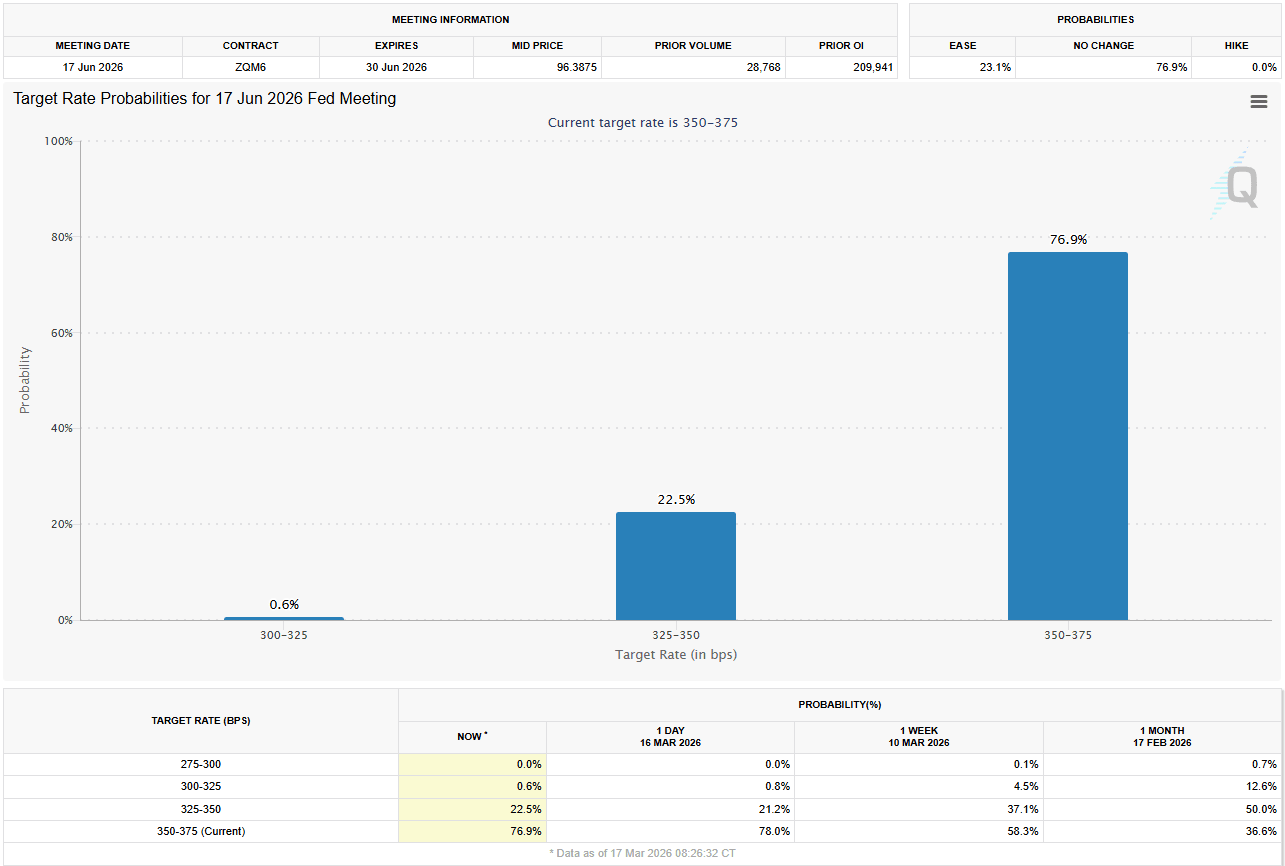

The CME FedWatch Tool shows that investors see virtually no chance of a rate cut in either March or April, while pricing in more than 75% probability of another policy hold in June. Actually, markets currently expect only one interest-rate cut this year, a big change compared to the three cuts anticipated before the breakout of the war in Iran.

What changed? The Fed will be conducting its meeting under extraordinary circumstances as rising crude Oil prices, due to the closure of the Strait of Hormuz amid the ongoing war between the United States (US) and Iran, heighten the uncertainty surrounding the inflation outlook.

DBS Group economist Philip Wee argues that the Fed enters its March 17-18 meeting caught between surging energy-driven inflation and weakening US growth.

“Fed Chair Jerome Powell may still be haunted by the “behind the curve” spectre of 2022, when a delayed response to surging prices forced a painful, aggressive hiking cycle,” Wee notes. This time, however, the Fed is currently confronting a fragile economy, he adds, citing the downward revision to the fourth-quarter Gross Domestic Product (GDP) growth and the 92,000 contraction recorded in Nonfarm Payrolls (NFP) in February.

“The FOMC must determine whether these energy price spikes represent a primary inflationary threat requiring higher rates or a consumer tax necessitating cuts,” Wee concludes.

Economic Indicator

FOMC Press Conference

The press conference is about an hour long and has two parts. First, the Chair of the Federal Reserve (Fed) reads out a prepared statement, then the conference is open to questions from the press. The questions often lead to unscripted answers that create heavy market volatility. The Fed holds a press conference after all its eight yearly policy meetings.

Read more.

Next release:

Wed Mar 18, 2026 18:30

Frequency:

Irregular

Consensus:

–

Previous:

–

Source:

Federal Reserve

When will the Fed announce its interest rate decision and how could it affect EUR/USD?

The Fed is scheduled to announce its interest rate decision and publish the monetary policy statement, alongside the SEP, at 18:00 GMT. This will be followed by Fed Chair Jerome Powell’s press conference starting at 18:30 GMT.

The rate decision itself is unlikely to trigger a significant market reaction, but investors will scrutinize the SEP and Fed Chair Powell’s tone.

The latest SEP, published in December, showed that the central bank’s projections implied a 25-basis-point (bps) rate cut in 2026, and another 25 bps reduction in 2027.

Additionally, Fed policymakers’ end-2026 projection for PCE inflation came down to 2.4% from 2.6% in September’s SEP. Given the recent rise in Oil prices, Fed officials are likely to point to higher inflation ahead.

The CME FedWatch Tool points to about a 30% chance that the policy rate will remain unchanged at the range of 3.5%-3.75% at the end of the year. In case the dot plot highlights that a majority of policymakers prefer to hold the policy steady for the rest of 2026, in addition to an upward revision to the end-2026 PCE inflation projection, the USD could gather strength with the immediate reaction and weigh heavily on EUR/USD.

Conversely, the USD could come under bearish pressure and allow EUR/USD to gain traction if the SEP points to at least one 25 bps reduction in rates this year.

Once markets digest the policy statement and the SEP, they will shift their focus to Powell’s presser, which will likely focus on fears about reviving inflation and his future at the Fed.

If Powell hints that they will have to prioritize controlling inflation and inflation expectations because of rising Oil prices, this could reaffirm expectations for a steady policy rate for longer and support the USD. On the other hand, the USD is likely to lose interest in case Powell doesn’t hit the panic button, noting that they will need more time to assess how the US-Iran conflict could influence inflation dynamics and that they will need to be more attentive to labor market conditions and support growth after seeing the sharp decline in February’s NFP.

“Powell will carefully avoid giving any strong forward-looking signals and emphasize the two-sided nature of the risks stemming from the energy supply shock,” said Danske Bank Research Team.

“Most FOMC participants still see the current policy rate level somewhat above neutral, and once the energy uncertainty eases, we expect the Fed to eventually deliver two more rate cuts in June and September,” they add. “Extending uncertainty could push the expected cuts further out into the future but not erase them completely, which we expect to be reflected also in the updated dots,” the analysts conclude.

Eren Sengezer, European Session Lead Analyst at FXStreet, provides a short-term technical outlook for EUR/USD:

“The near-term technical outlook points to a buildup in bearish pressure. The 20-day Simple Moving Average completed a bearish cross with the 50-day SMA and recently dropped below the 100-day and 200-day SMAs. Additionally, the Relative Strength Index (RSI) indicator stays below 40 after recovering slightly from the oversold region below 30.”

“On the downside, 1.1380 (Fibonacci 38.2% retracement level of the 2025-2026 uptrend) aligns as a key support level ahead of 1.1170 (Fibonacci 50% retracement). In case EUR/USD reaches the 1.1660-1.1700 region, where the Fibonacci 23.6% retracement, the 100-day SMA and the 200-day SMA form a strong resistance, technical buyers could take action. In this scenario, 1.1900 (round level, static level) could be seen as the next technical hurdle.”

Read the full article here